At Rotary Gallop, we believe that measuring the right thing, with the right tool is REALLY important!

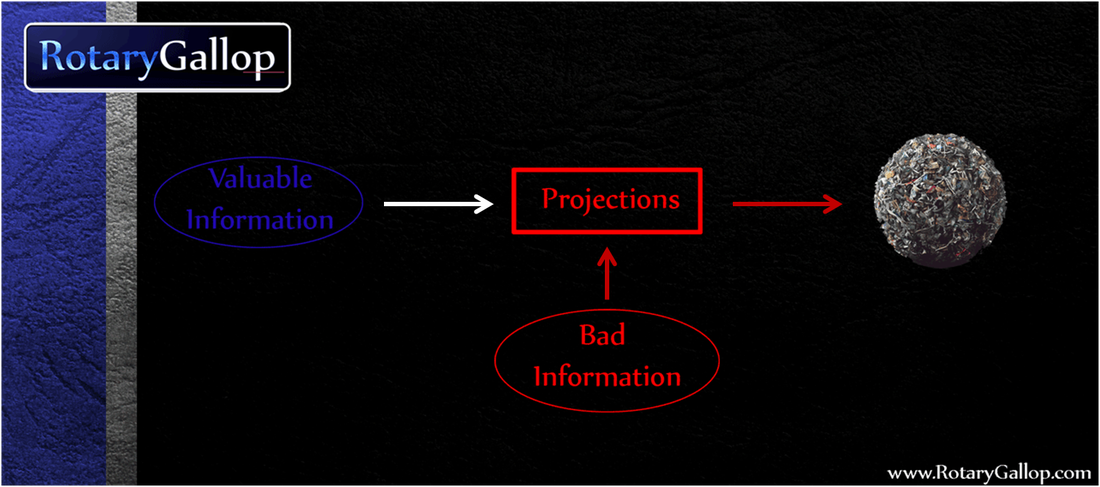

One of the biggest tragedies in the field of Investor Relations and Defense/Contested-Situation Advisory is one brought on by a terrible tool: Projections. Proxy solicitors popularized the name projections, but really all the experts we’ve talked to in the area of winning shareholder votes, (from successful activists, to Corporate Secretaries, heads of IR, IR consultants) are doing essentially the same thing. In fact, the problem described below is endemic to all analysis that involves starting at the top and working your way down a shareholder list (for convenience we’ll refer to all of this broader class as “projections”). Projections not only destroy useful information, but force people into measuring the wrong thing. These methods are wrong and destructive. So why is this terrible tool so wide spread? Because projections are intuitive and, in the absence of a better technology, were the only available choice.

What is wrong with Projections?

Your expert has LOTS of valuable information, which they generally use to predict a result (e.g. Projection - 63% of the vote For Managment). Unfortunately, the expert feeds this valuable information into their traditional method of analysis - projections. The problem is projections are inherently incapable of handling the vast number of outcomes (defined as combinations in which your shareholders might vote) possible in a shareholder vote! Projections are essentially a pencil and paper method that, with the help of an excel sheet and a really ambitions practitioner, might be able to consider, say, 100 different outcomes.

To drive home how inadequate this really is, below on the left is the number of atoms in the known universe. On the right are the number of unique outcomes possible in an election of just 1000 shareholders! A mind-boggling number!

One of the biggest tragedies in the field of Investor Relations and Defense/Contested-Situation Advisory is one brought on by a terrible tool: Projections. Proxy solicitors popularized the name projections, but really all the experts we’ve talked to in the area of winning shareholder votes, (from successful activists, to Corporate Secretaries, heads of IR, IR consultants) are doing essentially the same thing. In fact, the problem described below is endemic to all analysis that involves starting at the top and working your way down a shareholder list (for convenience we’ll refer to all of this broader class as “projections”). Projections not only destroy useful information, but force people into measuring the wrong thing. These methods are wrong and destructive. So why is this terrible tool so wide spread? Because projections are intuitive and, in the absence of a better technology, were the only available choice.

What is wrong with Projections?

Your expert has LOTS of valuable information, which they generally use to predict a result (e.g. Projection - 63% of the vote For Managment). Unfortunately, the expert feeds this valuable information into their traditional method of analysis - projections. The problem is projections are inherently incapable of handling the vast number of outcomes (defined as combinations in which your shareholders might vote) possible in a shareholder vote! Projections are essentially a pencil and paper method that, with the help of an excel sheet and a really ambitions practitioner, might be able to consider, say, 100 different outcomes.

To drive home how inadequate this really is, below on the left is the number of atoms in the known universe. On the right are the number of unique outcomes possible in an election of just 1000 shareholders! A mind-boggling number!

Atoms in the Known Universe: 100,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000 |  Possible Outcomes in a 1000 Shareholder Election: 1,000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000, 000,000,000,000,000,000,000,000,000,000 |

So, in order to reduce the number of outcomes to something manageable your expert is forced to start adding in shaky information, and eventually even making outright assumptions. If you mix good information with even a tiny amount of bad information, especially in a flawed methodology, the bad information wins every time. Thus the output of projections is garbage. “Garbage in – Garbage out” isn’t just a saying. It is an inarguable fact about our world, like the area of a triangle, resulting from the way errors propagate.

Garbage in - Garbage out: Projections force the use of shaky information, poisoning what solid intelligence is available and inevitably producing inaccurate results.

Your expert has spent a career building the expertise and connections that make up their incredibly valuable knowledge. It is precious. We should be protecting it from harm. Don’t let Projections ruin your experts most valuable assets! |

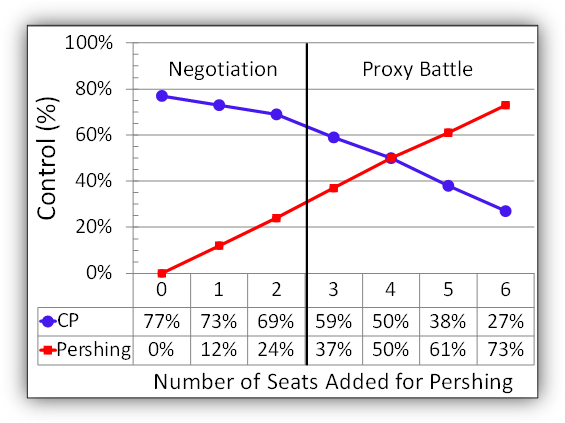

At Rotary Gallop, because we can handle the vast number of outcomes possible in your next shareholder vote, we can pool only the most certain information from all your experts and calculate useful, relevant, actionable intelligence - such as your control, your chances of victory, the control of each shareholder, and how much a given shareholder could change your chances of victory by siding for you or against you.

Next time I’ll explain how in addition to destroying your experts precious information, projections measure the wrong thing! It will be obvious once you see our latest innovation: The Map! If you have any questions email me at [email protected].

RSS Feed

RSS Feed